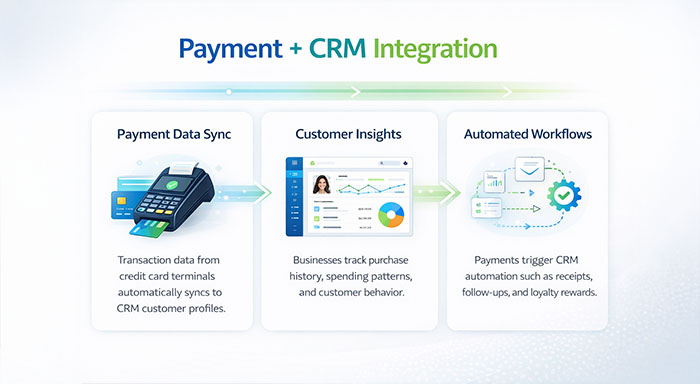

The clear disconnect between customer data and payment processes has frustrated businesses for a long time, making it difficult for them to understand their customers. Credit Card Terminal CRM Integration helps bridge this gap. When credit card terminals work independently from CRM platforms, organizations start to lose crucial transaction insights, experience duplicate entry of data, and miss vital opportunities to customize customer experiences. Integration easily resolves this disconnect, converting every payment into actionable intelligence while simplifying processes.

This shift is not just related to convenience. As payment technology evolves well and expectations grow, businesses that tether their payment infrastructure to their customer relationship management platform get a tangible benefit in both customer understanding and operational efficiency. Here is how to assess, execute, and streamline this integration for your business.

The Payment Process Technology Evolution

Credit card terminals have dramatically transformed from their origins as straightforward magnetic stripe readers. The devices today process contactless payments, chip cards, and mobile wallets while encrypting real-time data.

Modern terminals simultaneously provide support to diverse payment methods:

- EMV chip technology that creates unique transaction codes to prevent cloning of cards.

- NFC contactless readers for mobile wallets and tap-to-pay cards.

- Encrypted PIN pads that secure cardholders at the time of transmission.

- Cloud connectivity allowing data synchronization in real-time with business platforms.

This technological foundation ensures that integration with CRM platforms is just not possible, but greatly essential for businesses that are looking to leverage transaction data for customer knowledge.

Why Integration Ensures Trackable Business Value?

Linking payment terminals to your CRM ensures a closed loop between customer records and transactions. This integration removes manual entry of data, minimizes errors, and ensures instant visibility into customer purchasing behavior.

The operational advantages are substantial. Automating flow of transaction data into customer profiles, creates a comprehensive purchase history without intervention from staff. Payment confirmations kickstart CRM workflows, allowing automated follow-up communications. Customer service representatives see real-time payment status during support interactions. For organizations looking to level up this, integrating CRM with marketing automation can uncover in-depth efficiencies across the complete customer journey.

From a strategic point of view, integrated platforms showcase patterns that isolated data cannot be revealed. Businesses can recognize high-value customers as transaction amount and frequently, group audiences as per purchasing behavior, and tailor marketing as per real buying patterns instead of assumptions.

Choosing Hardware That Provide Support to Integration

Not all credit card machines provide the same capabilities of integration. When you are assessing options, emphasize devices with documented integration protocols and open APIs that align with your CRM system.

Important technical considerations involve the following:

- API availability: Powerful APIs that enable bidirectional flow of data between CRM and terminal.

- Security certifications: Point-to-point encryption and PCI DSS compliance to secure customer data.

- Support to Payment Method: Compatibility with emerging and current payment technologies.

- Connectivity options: Reliable internet connectivity through Wi-Fi, Ethernet, or cellular networks.

- Vendor ecosystem: Partnerships of integration with mainstream CRM systems and middleware providers.

Not all credit card machines provide the same capabilities of integration. When assessing options, providers such as DCC Supply, Verifone, and Ingenico each provide terminals with changing CRM compatibility and APi support. This is worth comparing your present stack before committing.

Apart from the hardware itself, assess the overall ownership costs, including monthly service charges, transaction fees, and integration maintenance costs. A marginally costly terminal with effective integration support generally delivers higher lasting value than a less costly device needing custom development work.

Security Architecture in Integrated Payment Systems

Integration improves the attack surface for possible breaches in security, increasing the importance of security protocols. Modern payment security depends on numerous protection layers operating together.

Encryption secures data in transit, converting confidential data into unreadable blocks of code from the moment the card is read until the moment the transaction is processed. Tokenization replaces actual numbers on card with randomly created tokens, ascertaining that even if a database is sacrificed, the stolen data cannot be utilized for fraudulent transactions.

EMV chip technology includes dynamic authentication, creating unique codes for every transaction that cannot be utilized. This ensures that card-related fraud becomes more trickier than with magnetic stripe cards.

For integrated platforms, additional measures of security involve:

- Role-driven access controls limit which staff members can see CRM payment data.

- Audit logging that monitors all access to confidential payment data.

- Secure storage of data with payment information grouped from general CRM data.

- Consistent security assessments to recognize as well as take care of vulnerabilities.

It is also important for businesses to maintain PCI DSS compliance, which establishes minimum standards of security for any organization that takes care of card payments. This involves access controls, network security, and consistent security testing.

Growing Technologies That Reshape Payment Processing

The payment landscape continues to rapidly evolve, with numerous technologies well positioned to modify how businesses process transactions and incorporate payment information.

Biometric authentication goes beyond smartphones into payment terminals themselves. Facial and fingerprint recognition can validate customer identity without needing devices or cards, minimizing fraud while expediting transactions. A few terminals now support palm vein recognition, which provides even greater security than fingerprints.

AI gets applied to real-time transaction data. Algorithms related to machine learning can detect unusual patterns of purchasing that can indicate fraud, highlight high-value customers for specific treatment, and forecast which customers are more likely to purchase products repeatedly. McKinsey analysis on payment trends recommends that AI-based payment platforms will become standard within the next few years.

Blockchain technology, while still growing in mainstream payments, provides potential for minimizing transaction costs and settlement times. Some payment processors are experimenting with blockchain-driven platforms that can allow near-instantaneous settlement while ascertaining transparency and security.

Specifically for CRM integration, such technologies allow richer collection of data and more advanced customer insights. Biometric data can connect transactions across devices, AI can segment customers automatically as per behavior, and blockchain can ensure immutable transaction records for dispute resolution and compliance.

Strategy for Implementation for Smooth Integration

Effective integration needs close planning and systematic implementation. Expediting the process generally leads to inconsistency in data, user frustration, and security gaps.

Begin by mapping your present customer and payment data flows. Record how transactions are processed currently, where customer information is stored, and what data needs to flow between platforms. This baseline understanding aids in recognizing integration points and possible complications.

Next, assess the capabilities of your CRM integration. Most CRM platforms provide native integrations with diverse payment processors or provide support to custom integrations via Application Programming Interfaces. Find out whether you will utilize a pre-developed integration, operate with a middleware platform, or create a custom solution.

The process of implementation generally follows the below-mentioned steps:

- Set up the payment terminal with the credentials of your processor and network settings.

- Set up API connection between CRM and terminal, including data mapping and authentication.

- Determine synchronization of data rules detailing which transaction details go to customer records.

- Establish automated workflows that cause payment events.

- Thoroughly test it with small volumes of transactions before completing deployment.

- Ensure staff training on new workflows and incorporated platforms.

- Track performance and make configuration adjustments as per real-world utilization.

At the time of testing, validate that transaction correctly appears in customer records; payment failures cause relevant alerts, and refunds update customer information properly. Test edge cases such as split transactions, partial payments, and payment plan strategies.

Staff training must cover both business advantages of integration and technical processes. Employees must understand not only how they can process payments, but how they can utilize the incorporated customer data to enhance service and recognize opportunities.

Enhancing Value from Incorporated Platforms

Integration generates opportunities that go beyond standard payment processing. Businesses that fully utilize integrated platforms leverage transaction data to optimize operations, improve customer engagement, and boost revenue.

Transaction history enables sophisticated customer segmentation. Identify customers by purchase frequency, average transaction value, product preferences, and seasonal buying patterns. Leverage such segments for personalized marketing campaigns that represent actual customer behavior instead of demographic assumptions.

Automated workflows caused by payment events can enhance operational efficiency and customer experience. Send customized thank-you messages after purchases, alert sales units when high-value customers complete transactions, or enroll customers automatically in loyalty programs as per the spending limits.

Payment data also gives visibility into operational insights. Assess transaction times to recognize bottlenecks, monitor payment method preferences to streamline checkout options, and track failed transactions to enhance authorization rates.

The Payment Intelligence’s Competitive Edge

As CRM platforms and payment technology become more advanced, the businesses that become successful are those that consider payment data as strategic advantages instead of transaction records. Integration changes credit card terminals from simple devices of payment into data collection points that improve customer understanding.

The technical implementation needs relevant hardware selection, strategic planning, and powerful security measures. However, businesses give value to in-depth customer insights, simplified processes, and tailored experiences. This justified the investment for organizations that are serious about customer relationships.

Begin by assessing your CRM capabilities and present payment infrastructure. Recognize gaps in customer visibility and data flow. Then, create a roadmap for integration that addresses technical needs while developing strategic business goals. The organizations that become experts in this integration will have a major edge in comprehending their customers as well as catering to them.

%201.png)

%201.png)

%201.png)