Privacy expectations are bringing paradigm shifts to how people approach online payment. As data breaches grow consistently, and cybersecurity measures become more prevalent, customers emphasize control, discretion, and minimum data exposure. This shift is encouraging merchants to reconsider compliance, payments, and trust. It can open new channels for businesses that quickly adjust and be more responsible in a privacy-driven digital economy.

Privacy-focused customers, "anonymous payments," and the business opportunity

Privacy-focused customers are not a fringe group or a single "type" of buyer. They're customers who make purchase decisions with one extra filter: how much personal information gets shared, stored, reused, or quietly repurposed after checkout. For them, payment privacy is part principle and part self-defense. They may still shop online, still use cards, still enjoy convenience. They just prefer choices that reduce the amount of data attached to a transaction—and increasingly, that can include using privacy‑oriented crypto through a reputable XMR exchange when it fits their needs.

In practice, "anonymous payment options" rarely means untraceable transactions. It usually means less personally identifiable data is collected, less data is retained, and fewer systems get to touch it. The business opportunity is straightforward: when privacy at checkout is handled professionally, it can increase trust, reduce abandonment, and shrink the company's data exposure at the same time. This approach is deliberately practical and compliant: understand what customers are protecting, choose appropriate anonymous payment options, implement controls that keep risk in check, and then measure what changes in conversion, support load, disputes, and customer sentiment.

Why privacy-focused customers prefer anonymous payment options

The trust gap: fear of misuse, tracking, and "data permanence."

Privacy-focused customers don't wake up wanting to be difficult at checkout. They're reacting to a modern reality: a purchase isn't just a purchase anymore. It's a data event. The item bought, the time, the location, the device used, and the identity tied to it can echo across ad networks, loyalty systems, and support tools for years. That lingering trail is what many customers mean by "data permanence." Even when the product is harmless, the feeling is the same: once the information exists, it can be copied, sold, breached, or misunderstood later.

Public sentiment supports that unease. A Pew Research Center survey found that about three-quarters of Americans say they have very little or no control over the data collected about them by companies, a concern that reflects the growing importance of data security and privacy in modern business. When customers feel that loss of control, they look for the simplest way to reduce exposure: fewer form fields, fewer accounts, fewer identifiers connected to the transaction. In payment terms, that often shows up as preference for anonymous payment options like cash in-store, prepaid payment options, or a "guest checkout" path that doesn't require a phone number, a saved profile, or a marketing opt-in just to pay.

Breaches and fallout: why customers reduce what they share

Breach fatigue is a big part of why customer data privacy concerns keep influencing payment behavior. Customers have seen enough headlines to internalize a blunt rule: any merchant could be the next one. That doesn't mean customers think every business is careless. It means they're no longer willing to bet their identity on it. When that mindset is in place, privacy at checkout becomes less about ideology and more about risk management. People reduce what they share because they can't control what happens after the "Submit" button.

There's also a business-side reason to take payment privacy seriously: breach economics. IBM's Cost of a Data Breach reporting put the global average cost of a data breach at $4.88 million in 2024. That figure isn't just a cybersecurity stat; it's a quiet argument for data minimization. Experts advise a practical posture: collect less personally identifiable information, store less sensitive data, retain it for shorter windows, and limit internal access. This lowers the "blast radius" if something goes wrong and reduces support chaos afterward. It also tends to improve the customer experience, which is an underrated side effect.

Fraud climate and defensive behavior

Rising payment scams and identity theft concerns add another layer. When fraud is common, customers change habits to feel safer and more in control, even if the method they choose is less convenient. The FTC reported that consumers lost more than $12.5 billion to fraud in 2024, a 25% increase from the prior year. In that environment, privacy-seeking behavior should not be treated as a red flag by default. For many customers, choosing more private payment privacy options is simply a way to avoid leaving a rich data trail, reduce exposure to account takeovers, and limit how much information can be used against them later. Businesses that recognize this-without getting naive about risk-are better positioned to keep trust and reduce checkout abandonment.

The market reality in 2025-2026: why payment privacy is not niche

Cash is still used and often preferred as a backup

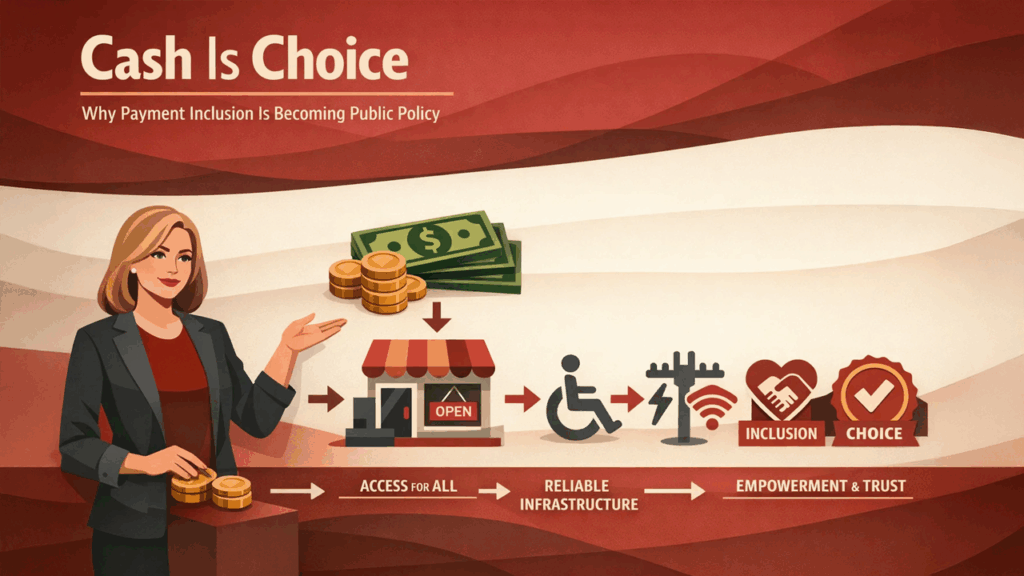

Payment privacy isn't a "crypto-only" topic, and it isn't limited to high-risk categories. It shows up in ordinary shopping behavior, especially where customers can choose how much data a purchase leaves behind. Recent Federal Reserve consumer payment research continues to show that cash remains a meaningful part of the U.S. payment mix, and that a large share of consumers keep cash on hand as a backup even when they pay digitally most of the time. In practical terms, cash is not just a payment method. It's a reliability tool and a privacy tool, and customers treat it that way.

That matters for merchants because a strict "cashless by default" posture can unintentionally filter out privacy-focused customers. It can also create inclusion issues for customers who are unbanked, underbanked, in between cards, or simply trying to limit data tracking concerns. From an operational perspective, accepting cash (where feasible) can be positioned as privacy and resilience: a customer choice that works when networks go down, phones die, or accounts get frozen after suspicious activity.

Policy signals: cash acceptance as consumer choice and inclusion

A second signal is that payment choice has become a public-policy issue, not just a merchant preference. Lawmakers at multiple levels have debated cash acceptance requirements, often framing cashless rules as exclusionary and risky during outages. There is also an ongoing federal interest in the topic, with proposals introduced that would push certain in-person retailers toward accepting cash rather than refusing it outright.

This should be treated as pressure in the direction of broader payment choice, not as a prediction that every business will be forced to accept every method. The safer takeaway is simpler: businesses that can support cash acceptance policies and other privacy-respecting options are moving with the direction of travel, while businesses that remove privacy-friendly methods may face increasing customer friction, reputational questions, and operational headaches when the next "systems are down" day hits. This is informational, not legal advice, and requirements vary by jurisdiction.

What "anonymous payment options" really mean: a practical spectrum

The spectrum model: anonymous, pseudonymous, and privacy-enhanced

Competitor content often uses "anonymous payments" like a magic label, but businesses benefit from a clearer internal model. A useful spectrum has three tiers.

Anonymous typically describes payments with minimal identity data attached at the point of sale. In most real-world commerce, this is closest to cash-like behavior in person. It's not "invisible to the universe." It's just low-data by design.

Pseudonymous describes payments where a transaction is tied to an identifier that is not a direct real-world identity, but can still become identifying over time. This is common in many digital contexts: accounts, wallet identifiers, or tokens that are consistent enough to link behavior even if the customer name is not front-and-center.

Privacy-enhanced describes payments that are not anonymous, but reduce exposure by limiting where sensitive information flows and how long it lives. Tokenization, minimized receipts, and shorter data retention windows often land here. This tier is where many legitimate businesses can make the biggest practical gains without crossing compliance boundaries.

Common options customers think of, and what each protects

Customers usually think of a few familiar buckets when they ask for anonymous payment options. Each protects something different, and each carries operational tradeoffs.

Cash is the clearest option for in-person privacy at checkout. It reduces the link between identity and purchase because it doesn't require a card account, bank account, or device identifier. The tradeoff is operational: cash handling procedures, theft controls, deposit logistics, and staff training. Best for in-person, low to mid ticket transactions, and businesses that can run basic cash controls without stress.

Prepaid payment options and gift card payments sit in the middle. Customers like them because they can limit exposure of a primary card and cap the amount at risk. The tradeoffs are fraud and support. Prepaid instruments can attract scams, and refunds can be tricky if policies are unclear. Best for online or in-person low to mid ticket purchases where the merchant can set sensible limits and clear refund rules.

Pay-by-bank methods can feel more private to some customers because they avoid sharing card numbers and sometimes avoid certain types of card-based tracking. The tradeoff is customer education, potential payment reversals in some contexts, and different dispute dynamics. Best for online transactions where customers are comfortable with bank-based checkout and where the merchant has strong reconciliation.

Digital wallet privacy is often misunderstood. Many wallets improve security and reduce direct card exposure to the merchant, which is good. But they are not necessarily anonymous. Wallet transactions can still create consistent identifiers and can still be linked across ecosystems. Best for customers who want fewer card details exposed to merchants, and for merchants who want lower data exposure.

How businesses can adapt: privacy-by-design payments that customers trust

Payment choice strategy: offer privacy-respecting defaults without hiding the ball

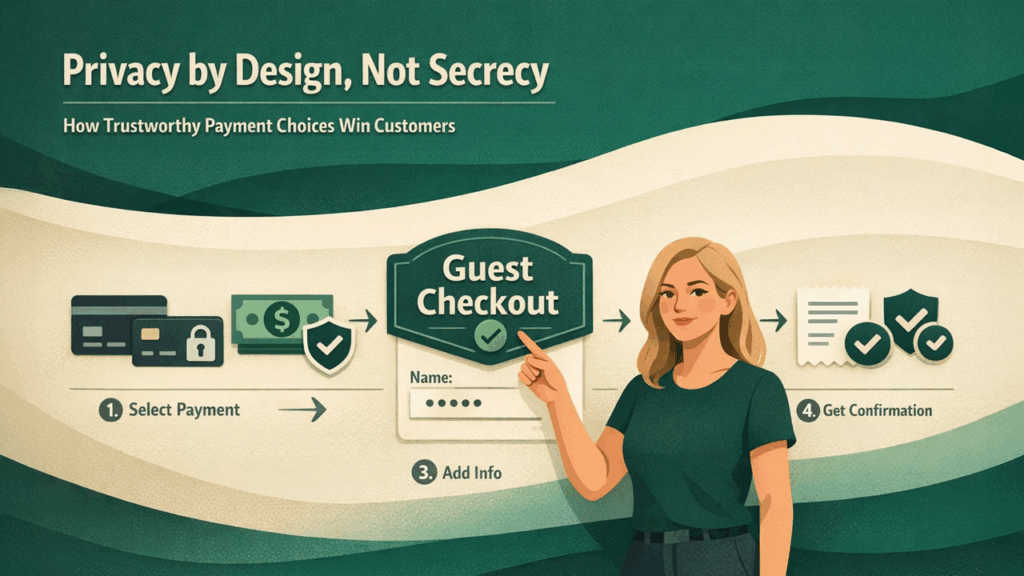

Privacy-friendly checkout isn't about acting secretive. It's about being calm, clear, and normal. Customers get suspicious when a merchant offers unusual payment options with vague language like "untraceable" or "no questions asked." That's not trust-building; it's brand damage waiting to happen.

TProfessionals recommend positioning payment choice as customer respect and security hygiene. Messaging can stay simple: "Multiple ways to pay, including cash in-store," "Guest checkout available," or "No account required." Receipts and confirmations can also reinforce professionalism: "Only the information needed to fulfill the order is collected," and "Marketing messages are optional." Short, plain language is better than a long privacy manifesto at checkout.

Data minimization at checkout: collect less, store less, retain shorter

Data minimization practices are where payment privacy becomes measurable. Many businesses collect personal data by habit: phone number required, account required, address required even for digital goods, or marketing consent bundled into the payment flow. Privacy-focused customers notice this immediately, and some will leave without complaining.

A practical shift is guest checkout by default, with optional account creation after purchase. Phone and email can be optional unless needed for delivery or service updates. Address capture should match the product: shipping requires it; a download usually does not. Retention can be shortened, and internal access can be reduced so fewer teams can view personal data. The operational benefit is real: fewer breach impacts, fewer "please delete my data" tickets, and less friction in support when customers challenge why certain fields were required in the first place.

Security that supports privacy: tokenization and reduced exposure

Payment tokenization is privacy-adjacent, not anonymous, and that distinction matters. Tokenization typically replaces sensitive payment data with a token so the merchant systems handle less raw card data. The customer still pays with a card account, but the exposure footprint changes: fewer systems can see sensitive data, fewer logs store it, and the overall risk surface shrinks.

For merchants, this can reduce PCI scope in some implementations and lower the blast radius if systems are compromised. For customers, it supports payment security by limiting how widely payment details circulate inside merchant environments. It's not a "privacy option" in the sense of hiding identity, but it's a strong move for payment privacy as customers often experience it: fewer unnecessary exposures, fewer reasons to worry about where card details end up.

Operational support: staff scripts, refunds, and dispute handling that don't punish privacy

Privacy-respecting checkout fails when operations punish the customer afterward. If a customer pays in cash or with a prepaid instrument and then learns returns are impossible, resentment builds fast. The fix is policy clarity, not policy generosity.

Define a cash refunds policy that is consistent and easy to explain: whether refunds are cash, store credit, or the original tender when possible. Receipt options should be flexible. Some customers want a printed receipt only; others want an email. Giving a choice reduces friction and supports customer service privacy. For disputes, staff should be trained to avoid demanding extra personal information as the default response. Basic guardrails help: clear proof-of-purchase rules, reasonable time windows, and escalation paths when unusual patterns show up.

Conclusion: the practical next step

Privacy-focused customers are optimizing for risk and control. They prefer anonymous payment options because those options reduce the identity trail connected to purchases and reduce exposure when the next breach or scam hits. This behavior is not inherently suspicious. It's a rational response to a world where personal data tends to spread, persist, and occasionally explode into a problem.

Businesses can adapt without turning checkout into a fraud magnet. The most reliable approach is to offer a reasonable payment mix, minimize unnecessary data collection, reduce retention windows, and implement controls that match the risk of each method. The practical next step is simple: run a 30-day checkout audit to identify privacy friction, then pilot one privacy-forward change (guest checkout default, clearer cash acceptance policy, or improved prepaid handling) and measure outcomes in conversion, disputes, refunds, and support. A business that does that consistently becomes the one customers trust when they care about payment privacy.

%201.png)

%201.png)

%201.png)