ShapeWhen you run a small business, you have to make multiple financial decisions at once. You manage inventory, handle invoices, watch payroll, and make strategies for next quarter while handling ongoing daily tasks. For many small business owners, cash flow is the thing that keeps them up at night and for good reasons.

As per recent research conducted by Bluevine and Centiment, nearly 4 in 10 small businesses struggle to cover more than a month of operating expenses when facing financial instability or disruption. That's a thin margin for error when a slow season hits; a customer starts delaying the payment, or an unexpected expense shows up.

The businesses that weather those moments best tend to have one thing in common: they didn't wait until they were in trouble to think about financing.

Cash Flow Problems Don't Always Look Like Emergencies

Most cash flow issues don't announce themselves. They creep in. A client who always paid on time stretches to 60 days. A supplier raises prices, and you absorb it quietly. You delay replacing equipment because the quote came in higher than expected. When in isolation. They don’t feel like a big deal, but together they chip away at your buffer.

When the realization hits owners about cash flow problems, they are barely left with any options. They would have more options to approach this problem if they identified this issue six months earlier. When lenders evaluate your application, they look at your recent financial history. Applying from a position of stability, before things get tight, gives you more leverage and better terms than applying under pressure.

Why Traditional Bank Loans Often Come Up Short

Banks become extra cautious when lending to small businesses, and it’s been always like this. They lay out strict requirements such as years of financials, strong credit, collateral, and a long process that takes about weeks or months. Traditional bank options feel limited for those business owners who can’t wait for months due to urgent need of capital or who has been in business under two years. That's where banks fall short.

That's where alternative lenders have stepped in. They provide assistance to those who own small businesses and whose profiles may not fit with traditional banks, but they own real and operating businesses with a decent, steady revenue. Their requirements start at a 500 FICO score, six months in business, and $15,000 in monthly revenue, without any prepayment penalties. It is a meaningful difference from what most banks offer. Being aware of these options is useful to those owners who get rejected by banks or are unwilling to go through a lengthy process.

The Financing Options Worth Understanding Ahead of Time

If you're going to be prepared, it helps to know what's actually available and what each option is for.

Lines of credit come handy in cash flow gaps and recurring needs. You take what is required, pay it back, and the credit replenishes. It is ideal for those businesses who have uneven revenue cycles or unpredictable timing on customer payments.

Short-term loans work well for specified needs with a clear timeline, covering payroll during a slow month, funding an order, or bridging a gap between a big receivable and a due date.

Equipment financing lets you acquire what you need without exhausting your cash reserves. In most cases, the equipment itself serves as collateral, so your requirements can be more flexible.

Invoice factoring is worth knowing if your business is actively involved in B2B work with long payment cycles. You can supercharge receivables with invoice factoring by selling outstanding invoices to a lender and getting most of the value upfront rather than waiting 30, 60, or 90 days.

These are not emergency measures; rather, they are tools that work better when you evaluate and think through them in advance. Do not rush to figure out when you're in the middle of the crisis.

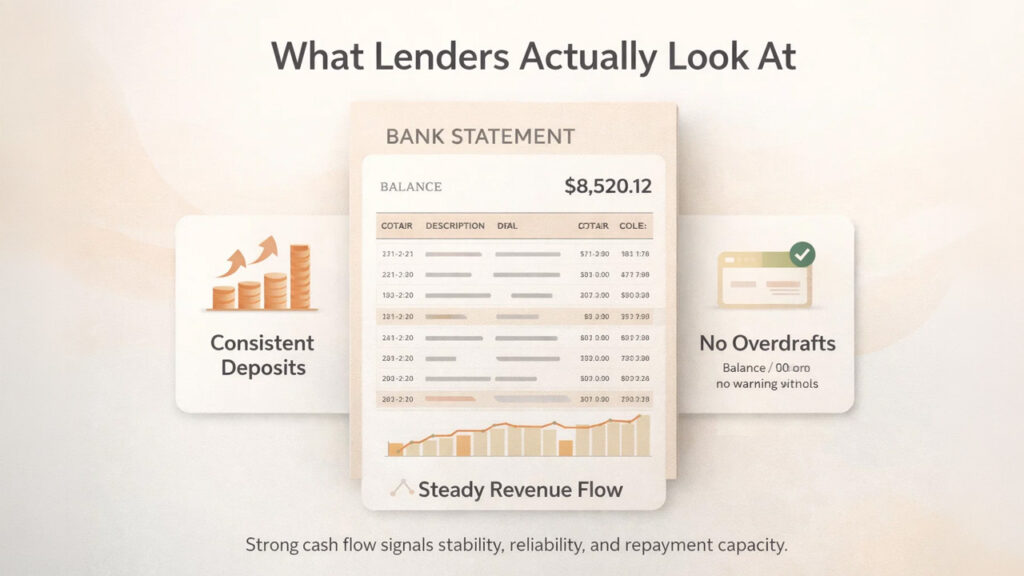

What Lenders Actually Look at

Cash flow is the single most critical financial metric for small business survival, with research consistently showing that the majority of small business failures trace back to poor cash flow management rather than lack of profitability. You can be making sales and still run out of cash if the timing doesn't line up.

Lenders know this, which is why they look closely at your business bank statements when you apply. They want to see consistent deposits, no recent overdrafts, and a pattern of steady revenue. The specific minimums vary by lender and product, but the underlying logic is the same across most of them: they're trying to understand whether your business generates enough cash to handle repayment without strain.

A few things that work in your favor as a borrower:

Your monthly revenue matters a lot. Most alternative lenders have a minimum they'll work with, and being clearly above that threshold strengthens your application.

Your FICO score sets a floor, not a ceiling. Getting above the minimum means you qualify. Getting well above it means you may have access to better terms.

Time in business matters for first applications. The longer you've been operating, the more data a lender has to work with. If you're newer, finding a lender whose minimums fit your situation is more important than trying to meet stricter requirements.

The Right Time to Apply

There's no perfect moment, but the practical answer is: before you urgently need it. An application filed from a position of financial stability tends to go better than one filed when things are tight. Your bank statements look better. You have more runway to compare offers. You're less likely to accept terms you'll regret.

Some owners build a line of credit specifically to have available before they need it, treating it like a financial cushion rather than a last resort. That approach takes some of the panic out of slow months or unexpected costs.

If you're thinking about your options and want to understand what the qualification process actually looks like, spending twenty minutes understanding the requirements at a few different lenders is time well spent. The landscape has changed a lot over the past decade, and for business owners who don't fit the traditional bank mold, there's more out there than most people realize.

%201.png)

%201.png)

%201.png)