Ever looked at your figures and wondered where the money went? Do you know what you own, what you owe, and how much cash is tied up, or do you rely on guesswork? Do you even use a business balance sheet? Remember, A healthy bank balance can hide late-paying customers, slow-moving inventory, or growing debt — none of which appear until you look at the full balance sheet.

This article will help you gain control of your business finances. It explains what balance sheets are, why having one matters, and how to prepare and review them so they work for your business.

What is a Balance Sheet?

A balance sheet simply is a snapshot showing a business’s financial position in three parts:

- Assets: These are anything the business owns outright, such as cash, equipment, inventory, and unpaid invoices.

- Liabilities: These are what the business owes: loans, unpaid bills, taxes, and payroll obligations.

- Equity: This is what is left over after the liabilities are subtracted from the assets.

This is what happens on the business balance sheet, expressed as one core formula:

Assets = Liabilities + Owner’s Equity By applying this formula, A=L+OE, a business balance sheet instantly shows what the business owns and what it owes, and, therefore, what is due to the owner as equity.

So, what is a balance sheet useful for? As the name suggests, it’s useful for understanding how closely income and outgoings balance at any point in time. To be ‘in balance’ would mean both sides of the equation match.

Why a Business Balance Sheet Matters

Unlike an income statement, which tracks revenue and expenses over time, or a cash flow statement that shows money moving in and out, a business balance sheet shows the here and now. At a glance, business owners know if there’s money for the next bill or when taking on debt is risky. More than that, a company's balance sheet reveals financial stability. It means it becomes easier to see whether the business is building value or whether liabilities are growing faster than assets.

All this makes a balance sheet a practical document that lenders, investors, accountants, and potential buyers expect to see. It goes beyond providing numbers and answers serious questions about the business. For example:

- Is the equity increasing or decreasing?

- Does the business generate enough cash to cover short-term and long-term expenses?

- Is the debt growing faster than it can be serviced?

- Can the business afford to expand, invest in new equipment, and hire more staff?

- How much pressure do unpaid invoices actually create?

Know The Balance Sheet Format

The balance sheet format is a point-in-time snapshot that follows the A = L + OE formula. It uses vertical columns, which are easier to organize and read; the first column lists Assets, divided into Current and Non-current.

Current assets include:

- Cash, accounts receivable, and inventory expected to become cash within a year

- Any prepaid expenses and unpaid invoices

On the other hand, non-current assets are long-term resources like property, vehicles, or paid-for equipment.

The next section is the Liabilities, divided into:

- Short-term, as a debt that is expected to last less than a year

- Long-term, as obligations lasting over a year (like a vehicle loan or equipment hire)

The final column on the balance sheet is the Owner’s Equity.

The result is a well-structured business balance sheet that lists the business’s assets and obligations. At the same time, it distinguishes its short-term financial pressures from its long-term ones.

Assets to Include

Now that you understand the balance sheet format, here's what to include under each category, starting with assets. Effective Asset Management ensures that every asset is accurately valued at its current worth rather than its initial purchase price, helping maintain a reliable and up-to-date balance sheet.

The most commonly listed assets are :

- Cash

- Accounts receivable

- Inventory

- Prepaid expenses

- Equipment

- Vehicles

- Property

- Long-term investments

Liabilities to Include

Liabilities should be listed on the balance sheet in the order of urgency or when they come due.

Listed liabilities include:

- Accounts payable, for example, payments due to suppliers

- Short-term loans

- Credit card balances

- Wages payable

- Lease obligations

- Long-term debt

- Deferred revenue, payments for goods or services that are still to be delivered

Owner’s Equity

The equity the owner is due is what remains after subtracting the value of all Liabilities. This should include both long- and short-term liabilities, subtracted from the value of all Current and Non-Current Assets.

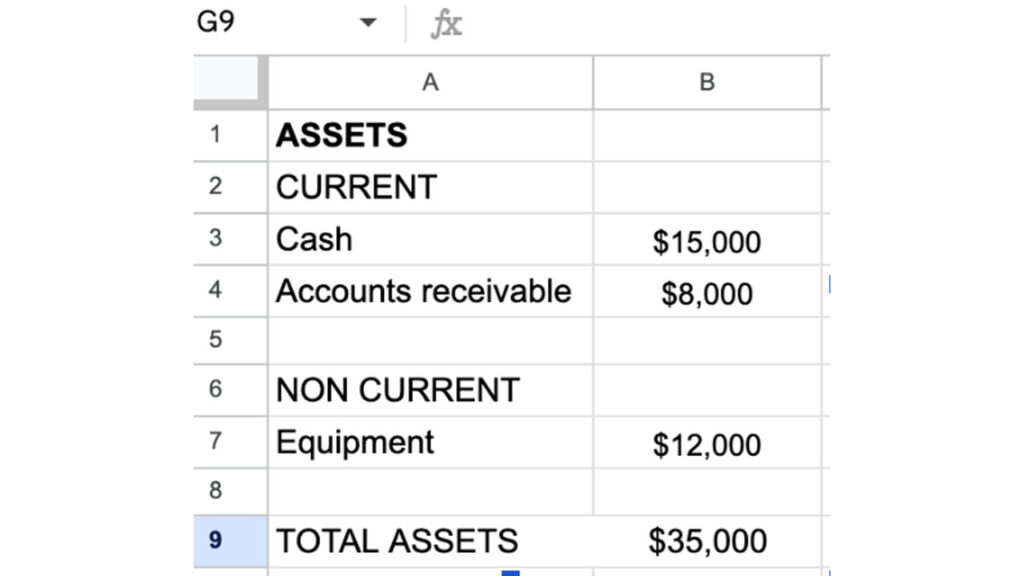

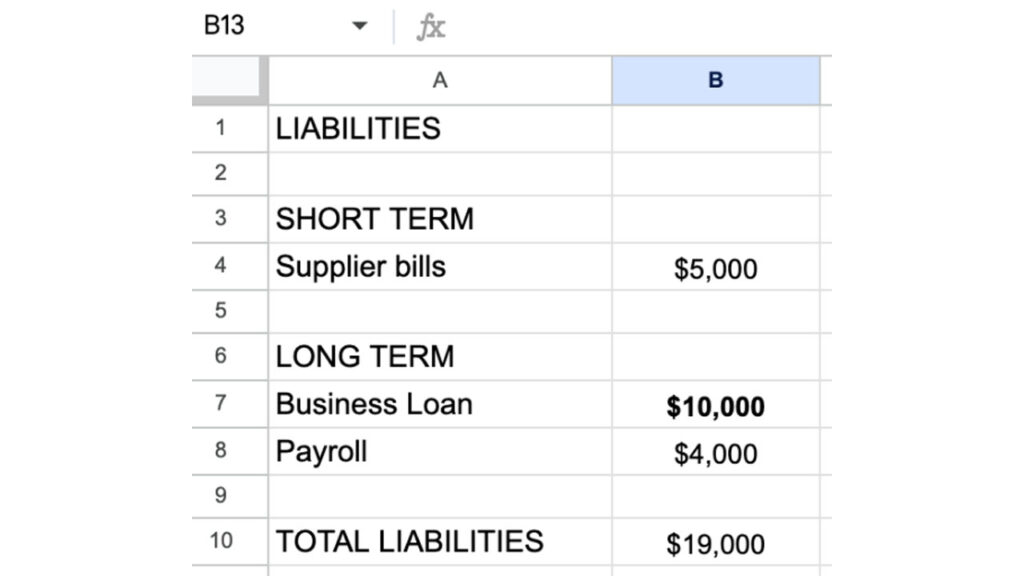

Simple Balance Sheet Example for a Small Business

This simplified example will help you visualize the layout of a balance sheet.

To keep the sheet consistent, the Liabilities must be listed in the same way.

Following the balance sheet format makes it simple to apply the OE=A-L formula to calculate the owner’s equity. In this example, owner’s equity is $35,000 minus $19,000, i.e., $16,000.

Note: This figure ($16,000) assumes all assets and liabilities were listed and that those listed were given their correct monetary value.

Keeping Balance Records Organized Before You Prepare One

Before preparing a business balance sheet, owners need to collect every document that supports the numbers. These typically include bank statements, unpaid invoices, loan agreements, supplier bills, inventory reports, tax summaries, equipment receipts, and previous financial summaries.

When these files are scattered across folders or saved in different formats, reviewing them with an accountant, lender, or business partner becomes unnecessarily difficult. Disorganized records also increase the risk of missing a figure that affects the final balance.

Bank statements and supplier invoices often arrive as PDF files. Rather than re-entering every figure by hand, you can convert a PDF to Excel using WordPDF, pulling the numbers directly into a spreadsheet. This reduces manual entry errors and makes it far easier to cross-check totals before passing your records to an accountant.

How to Make Balance Sheet Records Step by Step

Step 1. Choose the Reporting Date

Before making a balance sheet, select a specific date, typically the end of a month, quarter, or year.

Unlike income statements over a year, the balance sheets show activity as of a specified date. For most small businesses, quarterly preparation is sufficient, though lenders and investors will usually request one before any funding conversation.

Step 2. List Business Assets

Not listing an asset on the balance sheet is a critical mistake and leaves the business looking weaker than it is. You need to be thorough as you gather all the business’s resources together, and not forget to include:

- The inventory totals

- The equipment values

- Bank balances

- Vehicles and property

- Unpaid invoices

Step 3. List Business Liabilities

When considering how to prepare a balance sheet liabilities, record every debt the business carries, such as:

- Unpaid supplier bills

- Short-term loans

- Taxes owed

- Payroll obligations

- Credit card balances

- Lease payments

Separate them into short-term liabilities, due within a year, and long-term liabilities, such as vehicle loans or equipment finance, that extend beyond it.

Step 4. Calculate Owner’s Equity

Equity = Assets – Liabilities. Equity can be positive or negative here. If positive, it means the business owns more than it owes. Negative equity is not always a crisis when a new business invests in growth, but it is a good enough reason to review asset values and debt.

Step 5. Check the Balance Sheet Balances

The balance sheet, explained simply, is that total assets must equal total liabilities plus owner’s equity. However, even when using the right balance sheet format, performing regular Balance Sheet Reconciliation helps identify discrepancies before they become major financial issues, as there could be several reasons why the totals don’t match:

- A missing or duplicated entry

- Outdated numbers

- Incorrect calculations

- A misclassified account

Step 6. Compare With Previous Periods

A single business balance sheet is useful, but a collection updated on the same date each month holds valuable insights. Taken together, they reveal trends like:

- A rising amount of debt

- Shrinking cash reserves

- A growing inventory

- An increase in owner’s equity

Common Balance Sheet Mistakes Business Owners Should Avoid

A business balance sheet is only useful when it is accurate. Here are the most common mistakes to avoid:

- Personal and business finances mixed together. Personal transactions distort every figure and make the balance sheet unreliable for any external review.

- Unpaid customer invoices left off the list. Receivables are assets. Their absence makes the business appear weaker than it is.

- Supplier bills or tax obligations not recorded. These liabilities will surface eventually and reduce equity when they do.

- Inventory values that no longer reflect reality. Stale figures overstate assets and give a false picture of financial health.

- Assets recorded at purchase price rather than current book value. Vehicles and equipment lose value over time, and the balance sheet should reflect that.

It is also a mistake to rely on the balance sheet as the sole financial document that matters. It only reflects the financial condition at one point in time and does not capture any revenues, expenses, or cash flows. To get a complete picture, it’s good practice to review it together with income statements and cash flow statements.

Conclusion

A well-explained balance sheet reveals the actual value of your company. You should understand what a balance sheet is, so you stop relying on your bank balance alone. Therefore, business owners must learn how to make balance sheet reviews a standard part of their monthly routine.

Key Takeaways

- How often: Update and review your figures monthly or quarterly to stay ahead of trends.

- Why: To identify if debt levels are becoming risky or if inventory is tying up too much cash.

- What to look for: Monitor asset growth versus liability reduction to gauge overall stability.

By focusing on a balance sheet and maybe reviewing it along with your income statements, you can replace guesswork with certainty and lead your company with total confidence.

%201.png)

%201.png)

%201.png)